AI Infrastructure Bottleneck Trade 2026: Chips, Power, Data Centers, and the Next Market Rotation

A retail investor and trader guide to how AI demand is shifting from GPUs to HBM, advanced packaging, grid power, cooling, and rack-space scarcity.

Introduction

A few things has happened in the market that drove this article:

The Situational Awareness LP 13F, which are 45 days delayed BTW. This means that it’s should serve as a reference rather than directional information.

People calling tops on memory and AI stocks in general.

This idea that we see more and more regular 10 sigma events (“this should only happen once every 100 years in the markets).

I thought I’d combine all of the above into 1 article.

The One-Line Take

The AI trade is no longer just “who sells the best GPU.” It’s about a broader bottleneck stack: wafers, HBM, advanced packaging, power equipment, cooling, grid access, energized data-center capacity, and contract-backed AI cloud capacity. The best trading edge is likely to come from tracking which bottleneck is binding now, which one is easing, and which companies are converting scarcity into cash flow rather than just announcing capacity.

What Changed

AI demand has become a physical infrastructure cycle. GPUs still matter, but the deployable unit is a powered, cooled, networked, contracted rack, not a chip in isolation.

CHIPS Act reshoring is real but incomplete. U.S. front-end capacity is improving, especially around TSMC Arizona, Intel, Samsung, Micron, Amkor, and SK hynix projects. The big gap remains advanced packaging and HBM scale.

Hyperscaler capex is the demand umbrella. Microsoft, Alphabet, Amazon, Meta, and Oracle can fund massive buildouts, but investors need to test whether capex and RPO become profitable revenue.

Power and rack-space names are moving into the center of the trade. Bloom Energy, CoreWeave, Digital Realty, Equinix, Vertiv, Eaton, GE Vernova, Quanta, and miner-to-HPC names show why “electrons plus land plus interconnection” may be the next scarce asset.

This is a crowded, high-beta theme. The market-structure report is a useful warning: when a hot theme is financed, levered, option-hedged, ETF-linked, and sentiment-sensitive, price moves can overshoot fundamentals fast.

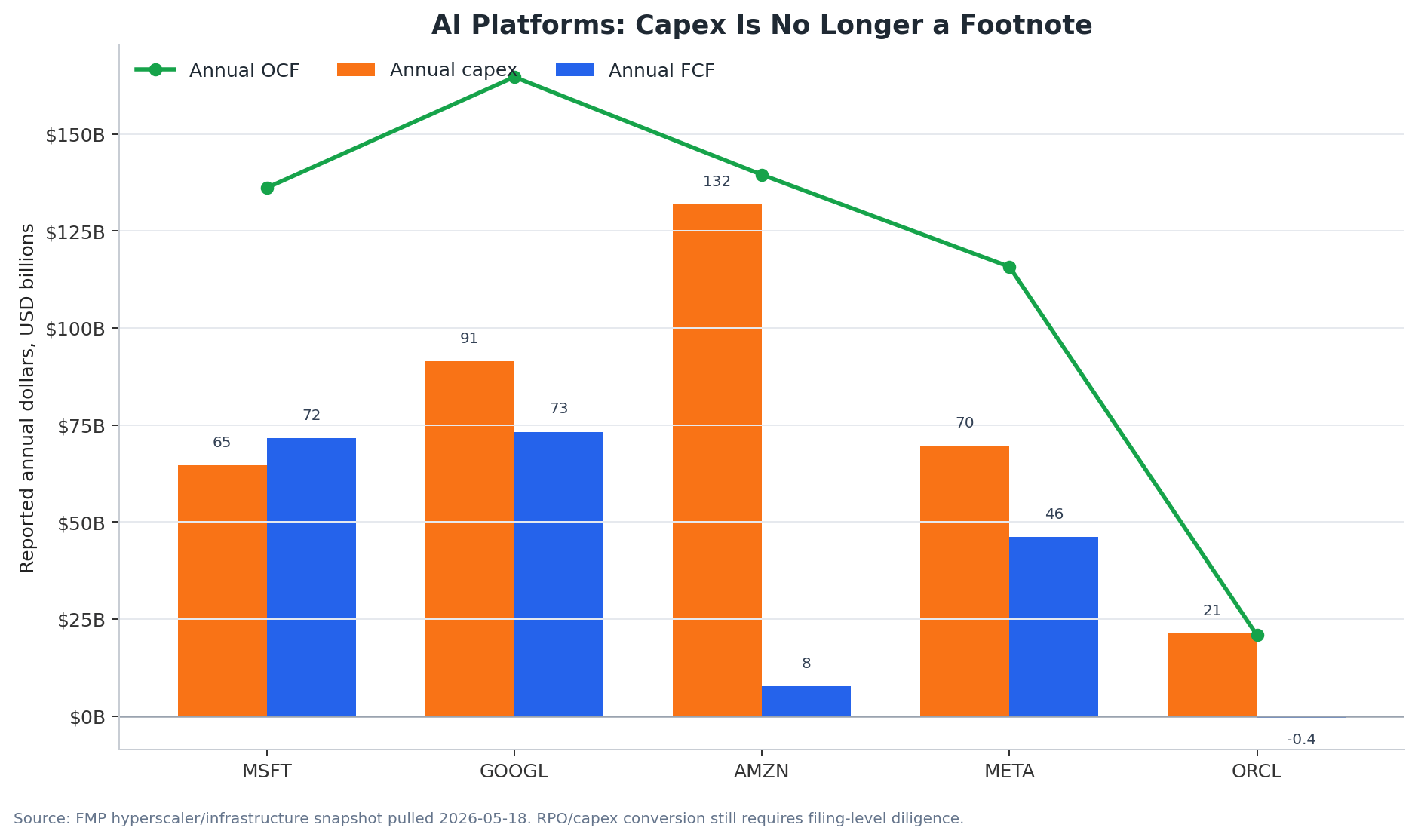

Chart 1: The Platforms Can Spend, But Returns Must Show Up

The hyperscaler chart shows why this cycle is so powerful and so risky. Microsoft, Alphabet, Amazon, Meta, and Oracle are spending at infrastructure scale. The bullish interpretation is that the largest buyers can self-fund AI capacity. The bearish interpretation is that capex, depreciation, and RPO conversion are now the real earnings test.

Trader read: If capex guidance rises while cloud margins hold and AI revenue disclosures improve, the theme stays healthy. If capex keeps rising while FCF, cloud margins, or RPO conversion deteriorate, the trade can flip from “scarcity premium” to “overbuild fear.”

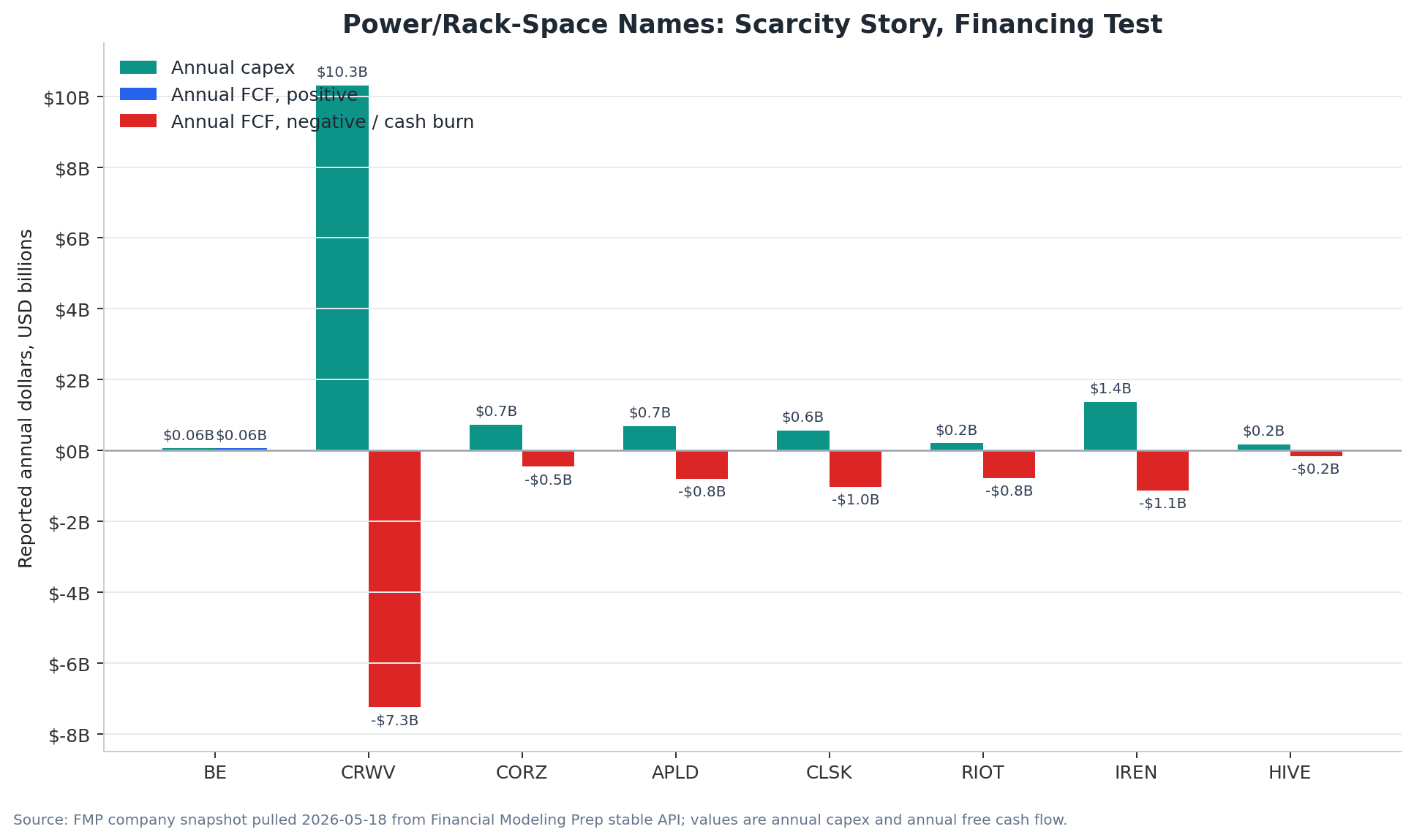

Chart 2: The Power/Rack-Space Cohort Is the High-Upside, High-Burn Layer

Bloom, CoreWeave, Core Scientific, Applied Digital, CleanSpark, Riot, IREN, and HIVE represent the physical bottleneck thesis in its most volatile form. They can benefit if secured power and energized sites become scarce. But the FMP data also shows the main problem: many names are capex-heavy and FCF-negative.

Trader read: Do not treat announced MW or GW as revenue. The signal is billing MW, contracted tenants, take-or-pay terms, financing cost, power pass-through, and gross margin after depreciation.

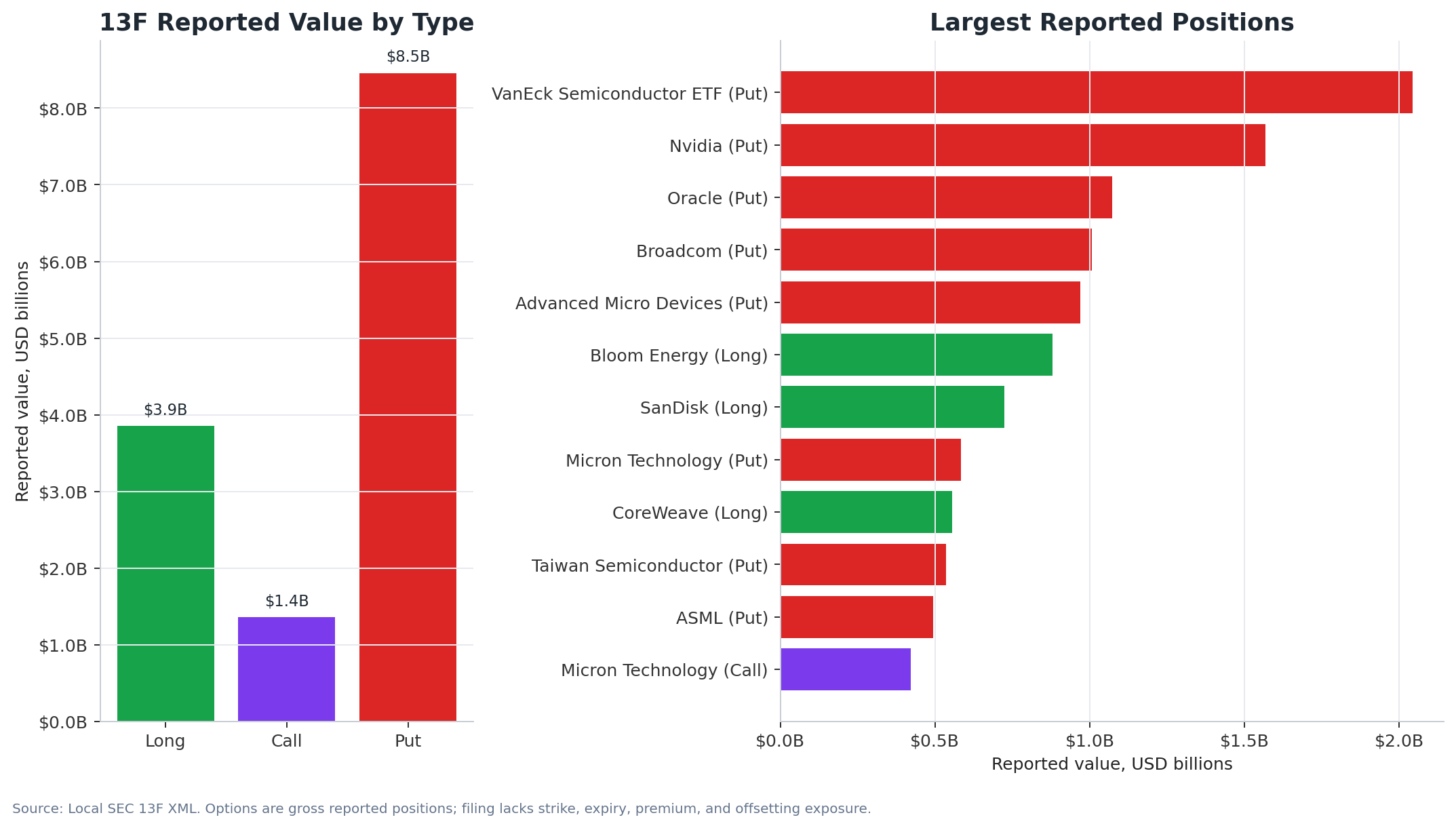

Chart 3: The 13F Looks Like Long Bottlenecks Plus Gross Puts

The Situational Awareness LP 13F shows large reported puts on semiconductor and AI beta exposures, but also large long exposure to Bloom Energy, CoreWeave, Core Scientific, Applied Digital, IREN, Riot, CleanSpark, and related physical-infrastructure names.

The clean read is not “bearish chips.” The better read is: long physical bottlenecks, hedge the crowded semiconductor/AI beta sleeve. 13F options data does not disclose strike, expiry, premium, delta, or offsetting positions, so the chart should be treated as signal, not proof.

Trader read: When a famous AI investor has puts on semis and longs on power/rack-space, retail should avoid simplistic narratives. The portfolio can be bullish the AI buildout and still hedged against Taiwan, capex, market beta, or valuation compression.

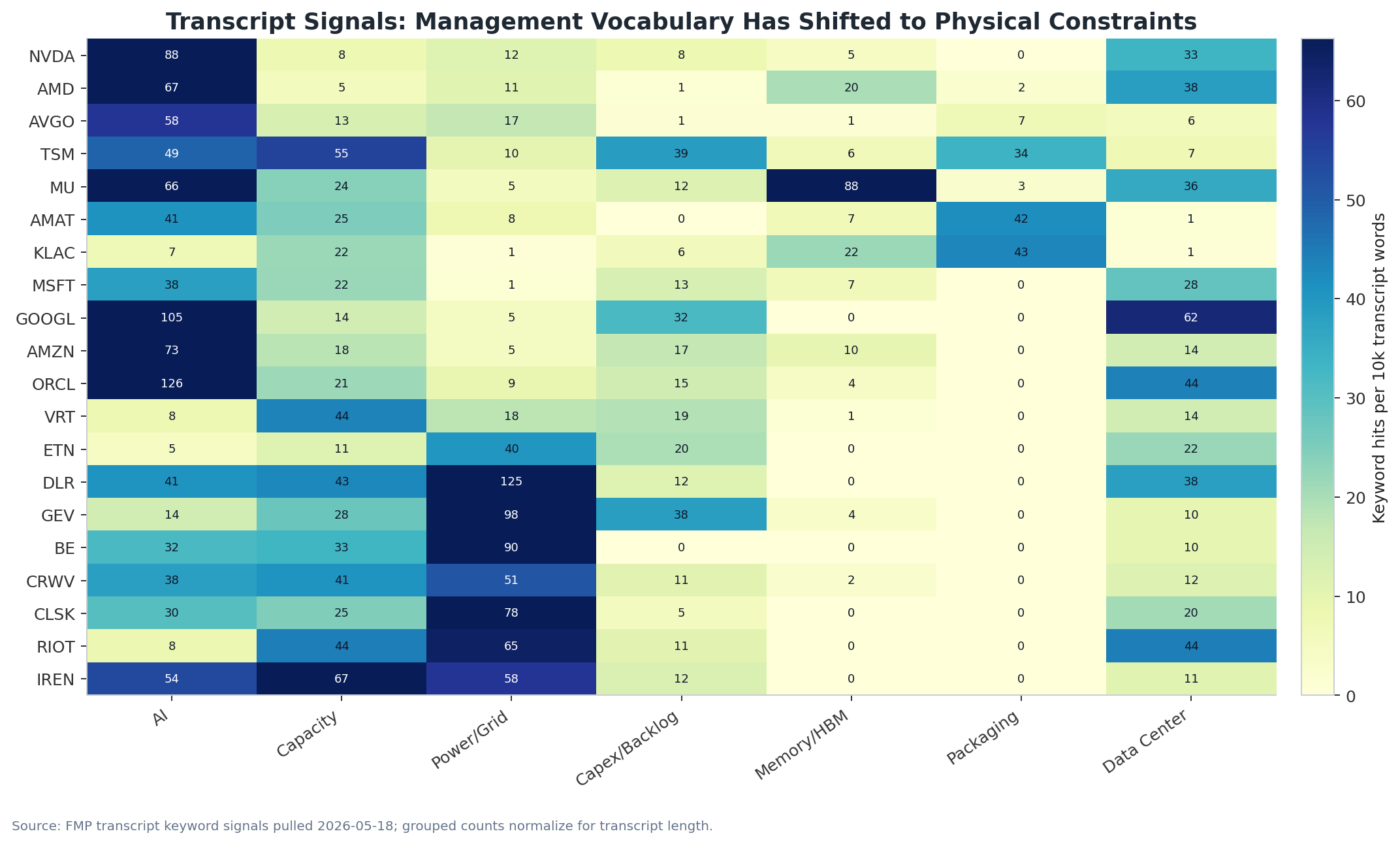

Chart 4: Management Teams Are Talking About the Same Bottlenecks

The FMP transcript signals show a clear vocabulary shift. AI is everywhere, but capacity, power/grid, capex/backlog, memory/HBM, packaging, and data-center language are now spread across semis, hyperscalers, power equipment, REITs, and miner/HPC names.

Trader read: The theme is broadening. If the next earnings season confirms more power, capacity, interconnection, packaging, and HBM constraints, the trade can keep rotating beyond the obvious chip leaders.

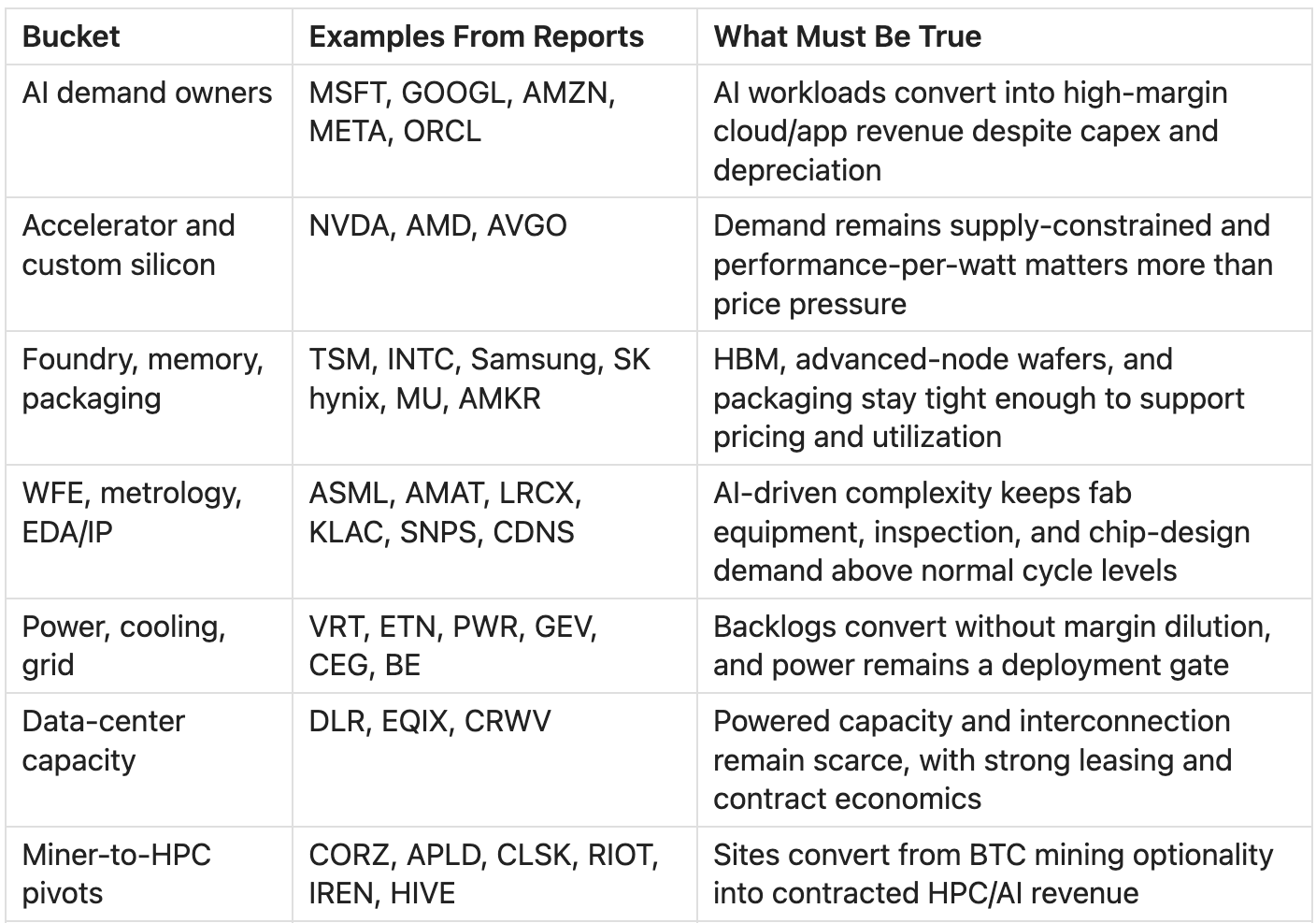

The Retail Watchlist Map

This is not a buy list. It is a map of what each bucket is supposed to prove.

The Trade Setup

Bull Case: Full-Stack Scarcity Persists

AI usage keeps growing faster than efficiency gains reduce compute needs. HBM, advanced packaging, power, and interconnection stay tight. Hyperscalers keep spending, cloud margins hold, and AI revenue disclosure improves. In this setup, leadership can broaden from NVDA/AVGO-style silicon into WFE, EDA, power equipment, grid, data centers, and select power-site owners.

Retail tactic: Favor companies with visible cash generation, backlog conversion, customer quality, and control of hard-to-replicate bottlenecks.

Base Case: Rolling Bottlenecks, Narrower Winners

The buildout continues, but the bottleneck rotates. Semis may cool while power heats up. Memory may tighten while server assemblers get squeezed. Some miner/HPC names execute, others dilute or miss schedules.

Retail tactic: Trade baskets by bottleneck layer. Do not assume every AI infrastructure ticker rises together.

Bear Case: Capex Air Pocket

AI capex slows, GPU/HBM lead times normalize, RPO conversion disappoints, financing tightens, and cloud margins compress. The market reprices the theme from “scarcity” to “overbuild.”

Retail tactic: Watch for the combination of capex cuts, slowing AI/cloud revenue, falling memory pricing, weak bookings, rising debt costs, and high VIX. That is when crowded names can gap before fundamentals fully show up.

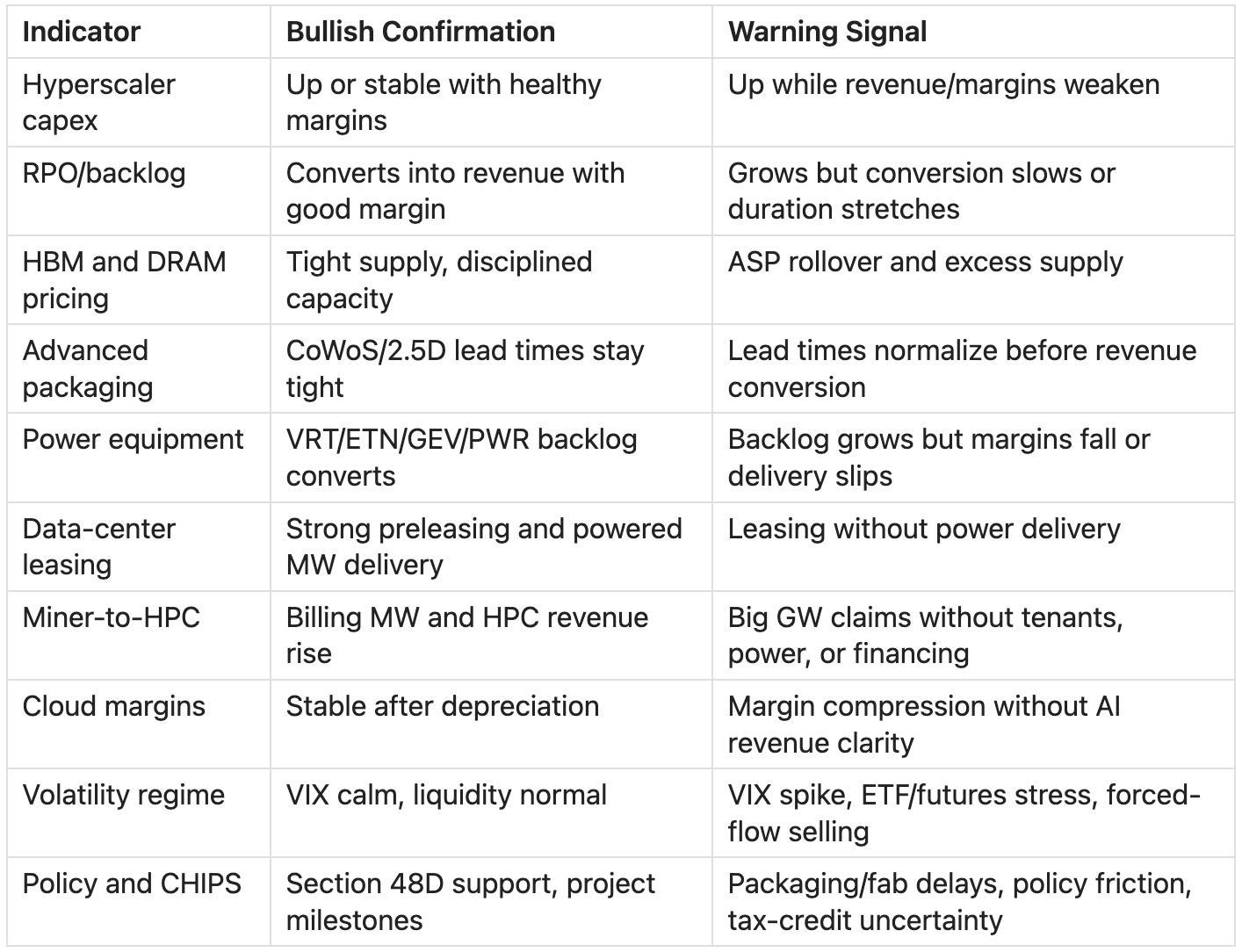

The Dashboard That Matters

Practical Retail Rules

Separate story from conversion. A company can have a great AI infrastructure story and still be a bad trade if it cannot finance the buildout.

Prefer evidence over announcements. Energized MW beats announced GW. Revenue beats RPO. Margin beats backlog. Free cash flow beats narrative.

Use different rules for different buckets. NVDA, ASML, Vertiv, Bloom, CoreWeave, and Riot are not the same trade. They sit at different points in the stack and carry different risks.

Respect valuation and volatility. The high-sigma report argues that crowded themes can move for market-structure reasons. If VIX rises and AI beta cracks, do not assume the first dip is automatically fundamental value.

Do not overread 13F options. Gross put value is not net short exposure. It may be hedge, spread, or tail protection.

Define invalidation before entry. Examples: capex cut, margin miss, tenant delay, financing stress, missed MW delivery, or HBM/pricing rollover.

Bottom Line

The investable AI theme is becoming an industrial capacity trade. Chips started it, but the next phase is about who controls the constrained layers that turn model demand into usable compute: HBM, packaging, power, cooling, grid access, and contracted rack space.

For long-term retail investors, the cleaner path is to focus on bottleneck suppliers and platforms with balance-sheet strength. For traders, the opportunity is rotation: semis when compute scarcity dominates, memory/packaging when integration bottlenecks dominate, and power/grid/data-center names when deployment becomes the constraint. The risk is that a crowded theme can unwind before the long-term story is disproven.