FUTU and TIGR Stock Crash Explained: China CSRC Crackdown, Fines, and the Two-Year Mainland Account Runoff

Why Futu Holdings and UP Fintech fell on May 22, 2026, what China's brokerage crackdown actually changes, and the signals that decide whether this is a one-time penalty or a bigger growth reset.

The One-Line Take

FUTU and TIGR did not fall just because China announced fines. They fell because China’s regulators are forcing a two-year runoff of affected mainland China brokerage accounts, and the market now has to decide whether Futu and Tiger are truly global growth platforms or still too dependent on China-linked cross-border trading.

TL;DR

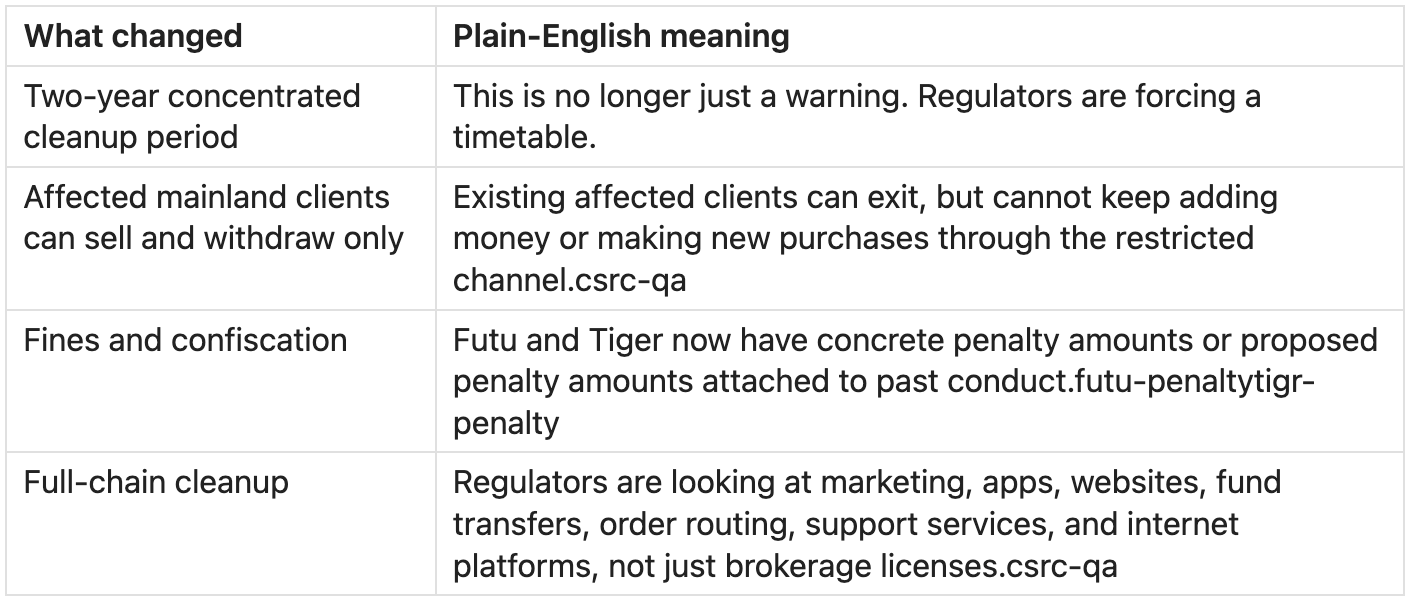

China regulators escalated a long-running crackdown on offshore brokers serving mainland China investors without proper domestic approval.

The key rule is simple: affected mainland clients can sell and withdraw, but cannot add money or make new purchases during the two-year cleanup period.[1]

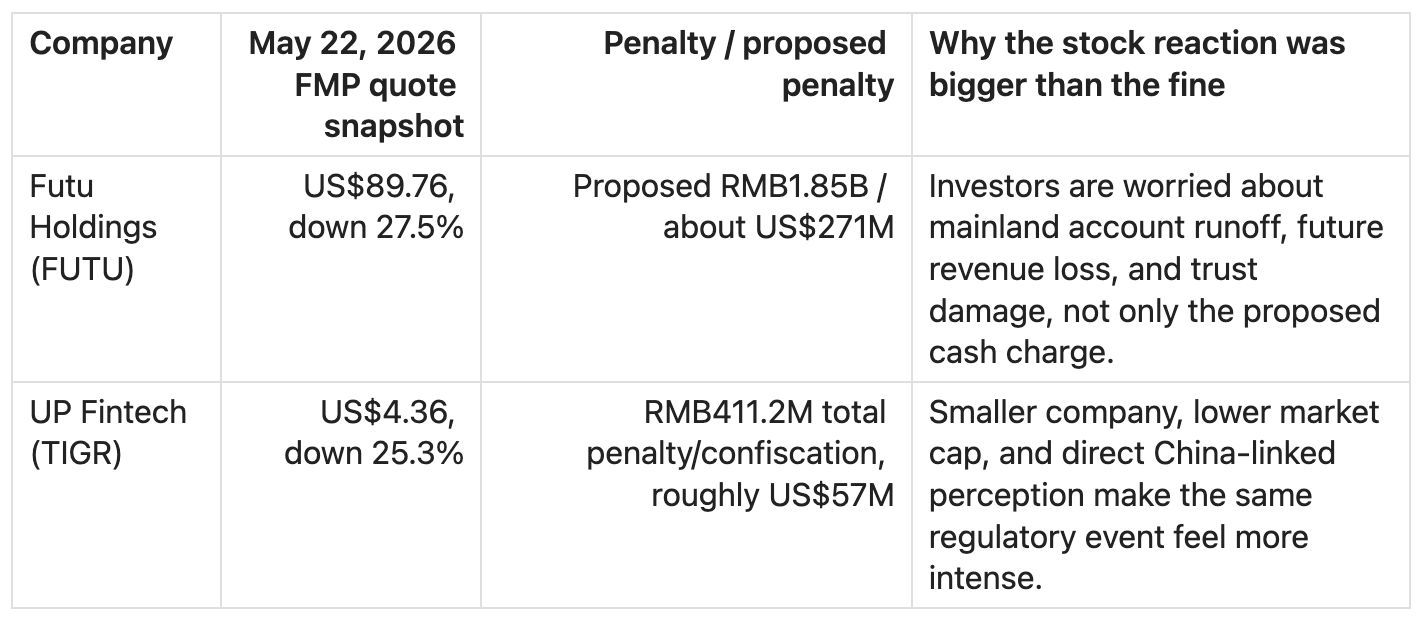

Futu disclosed a proposed penalty of about RMB1.85 billion, or roughly US$271 million, and said mainland China funded accounts were about 13% of total funded accounts at the end of Q1 2026.[2]

UP Fintech disclosed RMB308.1 million of penalties plus RMB103.1 million of confiscated gains, and said mainland China retail client assets were about 10% of total client assets at year-end 2025.[3]

On May 22, 2026, FMP quote data showed FUTU down 27.5% and TIGR down 25.3%.[4]

The debate is not “can they pay the fine?” The better question is “how much high-quality revenue disappears as mainland legacy accounts run off?”

The bullish interpretation: the crackdown clears an overhang and forces the companies to prove their Hong Kong, Singapore, Malaysia, Australia, Japan, and U.S. growth engines.

The bearish interpretation: the fines are only the visible part; the real issue is customer trust, revenue leakage, higher compliance cost, and lower valuation multiples.

What Happened?

On May 22, 2026, the China Securities Regulatory Commission and seven other Chinese agencies released a plan to clean up illegal cross-border securities, futures, and fund business.[5] This is not a brand-new issue. Back in December 2022, China had already told Futu and UP Fintech to stop taking new mainland investors through illegal cross-border channels.[6]

The 2026 action is different because it puts the cleanup into a more explicit two-year framework:

This matters because a brokerage account that can only shrink is not the same as a normal account. It may still generate some activity for a while, but it cannot compound through new deposits and new purchases.

Why Did FUTU and TIGR Fall So Hard?

The headline fines are large, but they do not fully explain the stock reaction by themselves.

The real market question: Are investors looking at a temporary cleanup cost, or the forced removal of a high-margin growth channel?

That is the whole trade setup.

Futu vs. Tiger: Quick Comparison

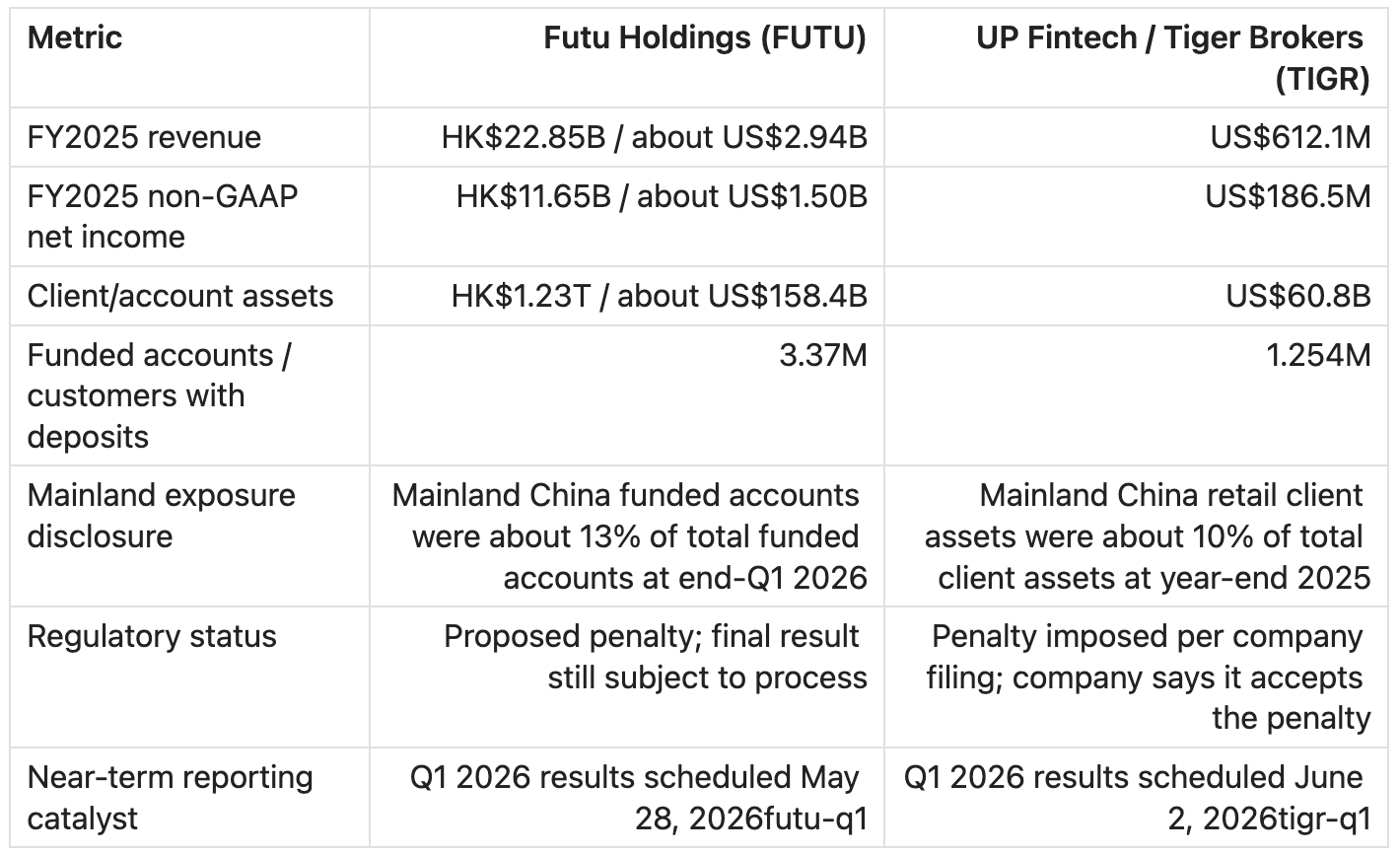

Retail translation: Futu is the bigger, more profitable platform with the bigger proposed fine. Tiger is smaller, cheaper-looking on some metrics, but the penalty and China narrative may feel heavier relative to its size.

The Simple Thesis

There are two ways to read the selloff.

The contained-damage view

FUTU and TIGR have already spent years expanding outside mainland China. Futu has moomoo in markets like Hong Kong, Singapore, Malaysia, Japan, the U.S., and Australia. Tiger has pushed Singapore, Hong Kong, Australia, and other international markets. If the mainland book is only low-teens exposure and runs off slowly, the selloff may have overreacted to a known regulatory issue.

What needs to be true:

Mainland revenue exposure is close to the disclosed account/asset exposure, not much higher.

International net new accounts and client assets keep growing.

Hong Kong and Singapore clients do not panic-transfer assets.

The final Futu penalty is not worse than the proposed amount.

Compliance costs rise, but do not destroy margins.

The bigger-reset view

The fines may be only the easy part to model. The harder part is whether the most active mainland clients were more profitable than average. If they used options, margin, IPOs, fund products, and frequent trading more than other clients, then a 10-13% exposure metric could understate the profit hit.

What needs to be true:

Mainland clients are higher ARPU than average.

Affected accounts sell down faster than expected.

Non-mainland clients start questioning platform safety.

Regulators outside China take a closer look.

The stocks keep a permanent “China fintech risk” discount.

What the Market Might Be Missing

Bullish miss: the fine is not the whole company

Futu and Tiger both reported strong FY2025 growth before the event. Futu’s FY2025 revenue rose 68.1%, funded accounts rose 39.6%, and client assets rose 65.9%.[9] Tiger’s FY2025 revenue rose 56.3%, customers with deposits rose 14.8%, and total account balance rose 45.7%.[10]

If most of that growth is now coming from outside mainland China, the market may be treating a shrinking legacy issue like a broken global franchise.

Bearish miss: funded accounts are not revenue

Futu disclosed that mainland China funded accounts were about 13% of total funded accounts. That does not tell us whether those accounts were 8%, 13%, 20%, or more of revenue. It also does not tell us whether they were high-margin users.

For Tiger, the 10% figure is client assets, not revenue. That is better than an account-count disclosure, but still incomplete.

This is the key retail investor trap: do not assume 10-13% exposure means exactly 10-13% earnings risk.

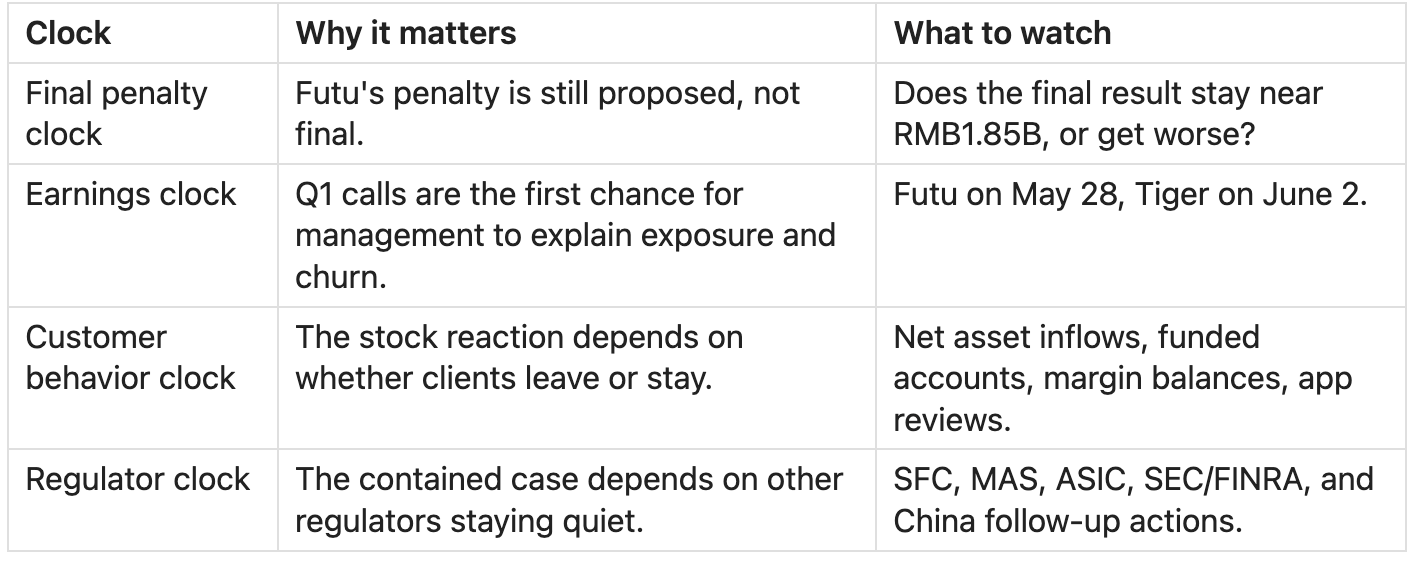

The Trader Setup

This is an event-driven setup with four clocks running at the same time.

For traders: The most important near-term data point is not the historical fine. It is whether management can give enough detail to calm the market on mainland revenue exposure, non-mainland account growth, and client asset retention.

For longer-term investors: The most important data point is whether these companies can keep growing client assets outside mainland China without giving back margin structure.

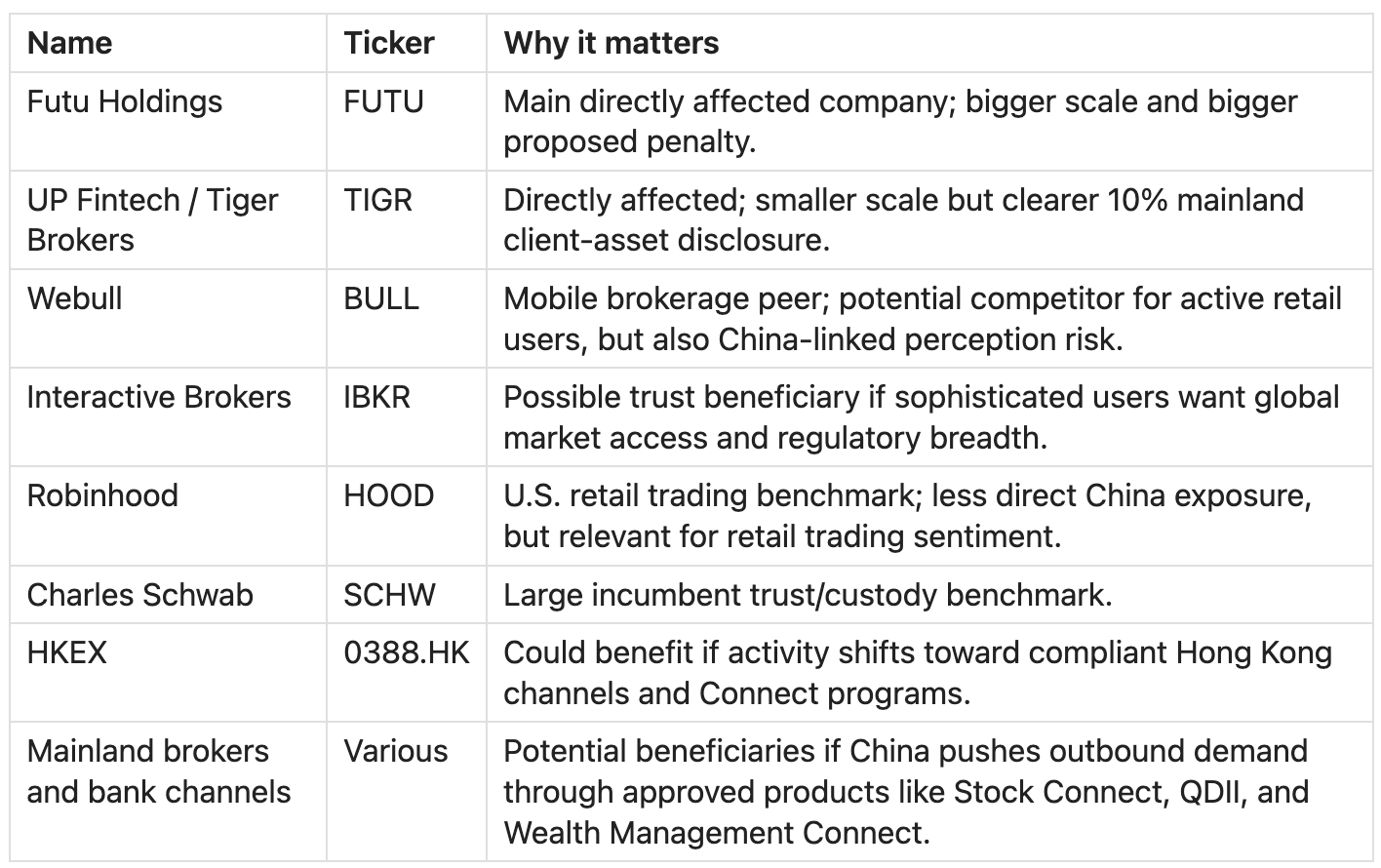

Watchlist: Winners, Losers, and Side Plays

This is not a ranked list. It is a research map.

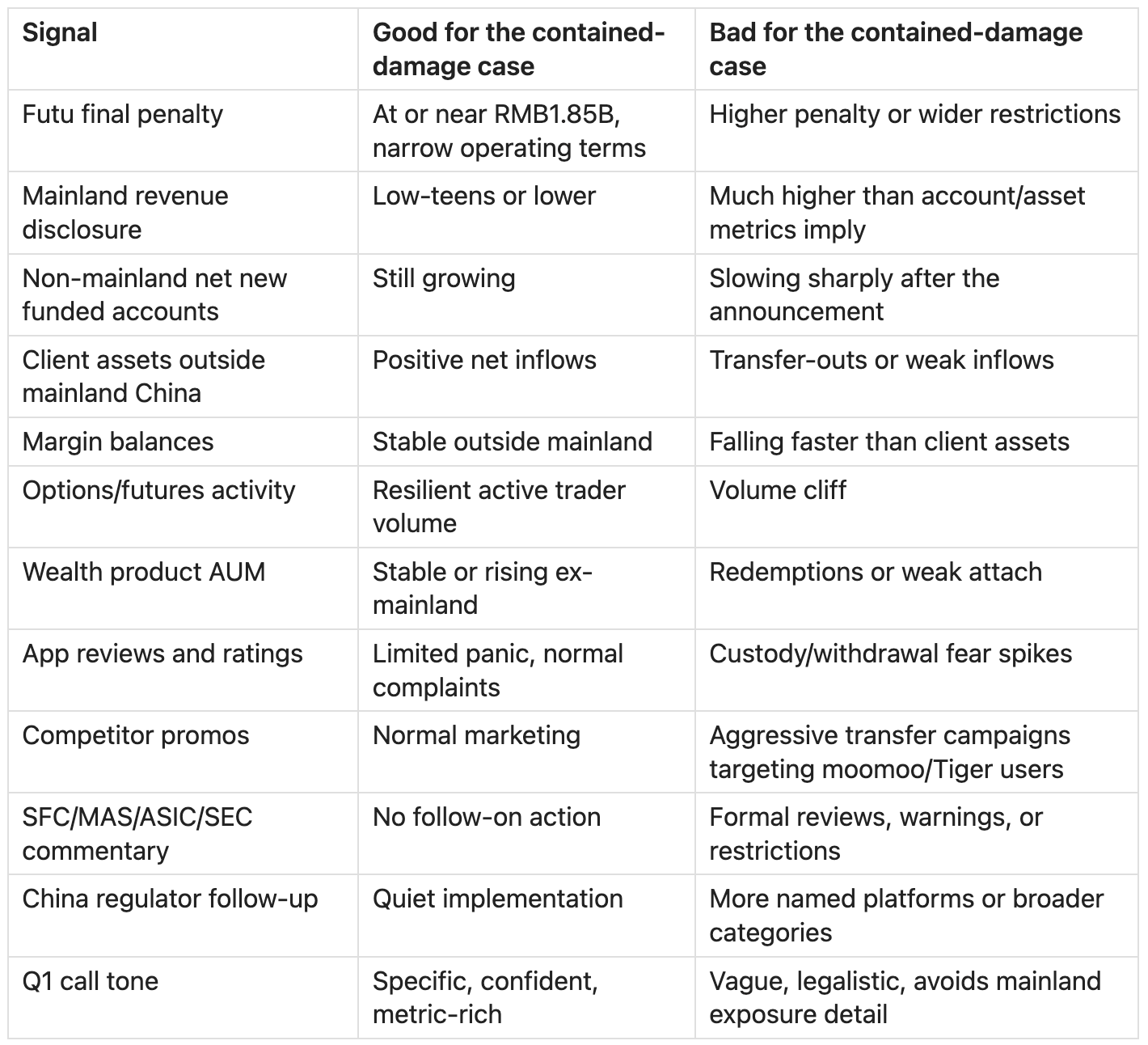

The Dashboard: 12 Signals to Watch

Three Scenarios

1. Clean runoff

Futu finalizes close to the proposed penalty, Tiger moves past the fine, and both companies show that international growth is still strong. Mainland accounts shrink, but the rest of the business keeps compounding.

What would support it: positive ex-mainland net asset inflows, stable margins, no foreign-regulator spillover, and detailed management disclosure.

2. Messy but manageable

The stocks remain volatile. Mainland revenue declines, compliance costs rise, and investors demand a lower valuation multiple. But the companies remain profitable and international growth offsets part of the damage.

What would support it: account growth continues but margins compress, management gives partial disclosure, and client trust outside mainland China holds up.

3. Trust break

Mainland clients exit faster than expected, non-mainland clients get nervous, and competitors take share. The market stops valuing FUTU and TIGR like global fintech growth stories and starts valuing them like China-regulatory-risk brokers.

What would support it: rapid asset runoff, weak Q1/Q2 operating metrics, vague calls, foreign regulator attention, or app-review panic.

What I Would Want to Hear on the Next Earnings Calls

What percentage of revenue, gross profit, margin balances, and trading volume came from affected mainland China accounts?

How quickly are affected mainland clients withdrawing assets?

Are Hong Kong, Singapore, Australia, Japan, and U.S. accounts still growing?

Are client assets outside mainland China seeing net inflows or outflows after the announcement?

What is the expected compliance and remediation cost over the next two years?

Has any regulator outside mainland China requested changes to operations?

Are margin balances, options volumes, and wealth AUM stable outside mainland China?

Can management explain exactly why non-mainland operations are ring-fenced?

If management answers these clearly, the market can model the damage. If management avoids them, uncertainty stays in control.

Bottom Line

For retail traders, FUTU and TIGR are now event stocks. The next move depends less on the already-announced fines and more on what management reveals about mainland revenue exposure, customer withdrawals, and non-mainland growth.

For retail investors, the core question is whether Futu and Tiger are still high-growth international brokerage platforms after China’s cleanup, or whether the market should permanently value them with a heavier China regulatory discount.

The most useful stance is not hype and not panic. It is a dashboard: final penalty, mainland runoff, international inflows, margin balances, and regulator spillover. Those five signals will tell the story faster than the headline fine amount.

Sources

China Securities Regulatory Commission, Q&A on the comprehensive rectification plan, May 22, 2026. https://www.csrc.gov.cn/csrc/c100028/c7634328/content.shtml↩︎↩︎↩︎

Futu Holdings Limited, Form 6-K, “Futu Receives Investigation Notice and Administrative Penalty Pre-Notification Letter from the China Securities Regulatory Commission,” filed May 22, 2026. https://www.sec.gov/Archives/edgar/data/1754581/000110465926065484/tm2615466d1_6k.htm↩︎↩︎

UP Fintech Holding Limited, Form 6-K Exhibit 99.1, “Administrative Penalty by the CSRC,” filed May 22, 2026. https://www.sec.gov/Archives/edgar/data/1756699/000119312526235622/tigr-ex99.htm↩︎↩︎

Financial Modeling Prep stable API quote and company-data pulls for FUTU, TIGR, BULL, IBKR, HOOD, and SCHW, pulled May 22, 2026 using the user-provided API key. Documentation: https://financialmodelingprep.com/developer/docs/stable↩︎

China Securities Regulatory Commission, “Comprehensive Rectification Plan for Illegal Cross-Border Securities, Futures and Fund Business Activities,” May 22, 2026. https://www.csrc.gov.cn/csrc/c100028/c7634326/content.shtml↩︎

CGTN, “China orders brokerages to cease illegal cross-border activities,” December 31, 2022. https://news.cgtn.com/news/2022-12-31/China-orders-brokerages-to-cease-illegal-cross-border-activities-1gdfvoboPkI/index.html↩︎

Futu Holdings Limited, “Futu to Report First Quarter 2026 Financial Results on May 28, 2026,” May 19, 2026. https://ir.futuholdings.com/news-releases/news-release-details/futu-report-first-quarter-2026-financial-results-may-28-2026↩︎

UP Fintech Holding Limited, “UP Fintech Holding Limited to Report First Quarter 2026 Financial Results on June 2, 2026,” May 21, 2026. https://ir.itigerup.com/news-releases/news-release-details/fintech-holding-limited-report-first-quarter-2026-financial↩︎

Futu Holdings Limited, Form 6-K Exhibit 99.1, Q4 and FY2025 unaudited financial results, filed March 12, 2026. https://www.sec.gov/Archives/edgar/data/1754581/000110465926026621/tm268330d1_ex99-1.htm↩︎

UP Fintech Holding Limited, Form 6-K Exhibit 99.1, Q4 and FY2025 unaudited financial results, filed March 19, 2026. https://www.sec.gov/Archives/edgar/data/1756699/000119312526115048/tigr-ex99_1.htm↩︎